Wired Differently: The VC Guide to the ADHD Alpha

Why the traits that get misdiagnosed in classrooms are the same ones building billion-dollar companies

25/02/2026

Marius Swart

Forget Silicon Valley's obsession with 'Genius.' The next wave of disruption is being built by the neurodivergent. With roughly 25-30% of self-employed founders meeting ADHD criteria, this article examines the complexities and the strategic investment opportunity presented by the high-performance ADHD cognitive profile.

The Breakdown: What are we actually talking about?

ADHD isn't just "being hyper." In 2026, we've moved past the deficit-only model. It's a double-edged sword — and it's important to name both edges honestly. For many people, ADHD is a genuine disability that causes significant daily impairment: lost jobs, strained relationships, and real suffering. At the same time, the same neurological profile that drives those challenges can also enable high-stakes crisis proficiency and divergent thinking that straight-line thinkers simply can't replicate.

We've been documenting this for 200 years, but only recently have we recognized there's no "blood test" for it. Diagnosis still relies on clinical evaluations of history and behavior. This diagnostic "bottleneck" is actually a significant investment opportunity — but to appreciate the scale, we must first understand the different components of the market.

The Market: By the Numbers (2026)

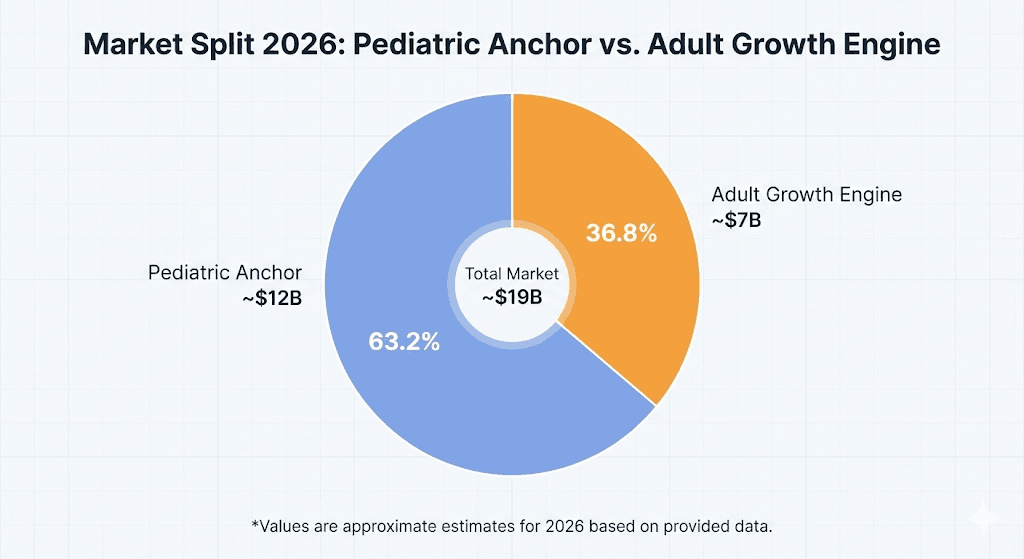

If you think ADHD is just a "kids' market," you’re missing the bigger opportunity. As of 2026, the sector is split into two massive, distinct opportunities:

The Pediatric Anchor: ~$12B. This is the bedrock of the sector, focused on ages 3-17.

The Adult Growth Engine: ~$7B. This is where the real "alpha" is for VC’s investing directly in ADHD solutions.

Why we think this is undervalued:

The C-Suite Disclosure: 44% of large orgs now have a senior exec who has publicly "come out" as neurodivergent. It’s becoming a corporate badge of honor.

The Founder Link: Roughly 25-30% of self-employed founders meet ADHD criteria.

Selection Bias: Fortune 500 leader traits: risk tolerance, high energy, and hyperfocus are ADHD traits. Think Richard Branson or JetBlue’s David Neeleman. These guys aren't outliers; they're the archetype.

Fact-Checking the Stereotypes

Forget the "kid who can’t sit still." In 2026, we look for the "Ferrari Engine (superpowers), Bicycle Brakes (systems or practical tools)" profile.

Here is the ground truth:

The Low Arousal Paradox: ADHD brains are actually under-stimulated. Stimulants (Adderall/Vyvanse) act like a "wake-up" signal so the brain can finally stop hunting for dopamine and just... focus.

Time Blindness: It’s not laziness; it’s Chronosagnosia. The brain perceives "Now" or "Not Now." This makes linear scheduling a nightmare, but makes them lethal in "sprint" environments.

Hyperfocus: The secret weapon. When the interest is there, the rest of the world (sleep, food, noise) vanishes.

The Gender Diagnostic Gap: Women and girls were missed for decades because they presented as "daydreamers" rather than "disruptive." This is a massive, underserved diagnostic market.

Ferrari Engine: The Superpowers (The Investment Thesis)

When you’re looking at a founder, you aren't looking for "normal." You're looking for these ADHD-driven edges:

Divergent Thinking: While most go A → B → C, these founders go A → Blue → Jazz → Space. That associative leap is where "disruption" actually comes from and directly leads to intellectual property that competitors, locked in linear thinking, cannot replicate or see.

Crisis Calm: Under-stimulated brains love chaos. When a startup faces an unexpected market shift, the ADHD founder is finally at their baseline and shows remarkable resilience by avoiding decision paralysis.

Pattern Recognition: They are "floodlights," not flashlights. They see the whole room (and the market shifts) at once.

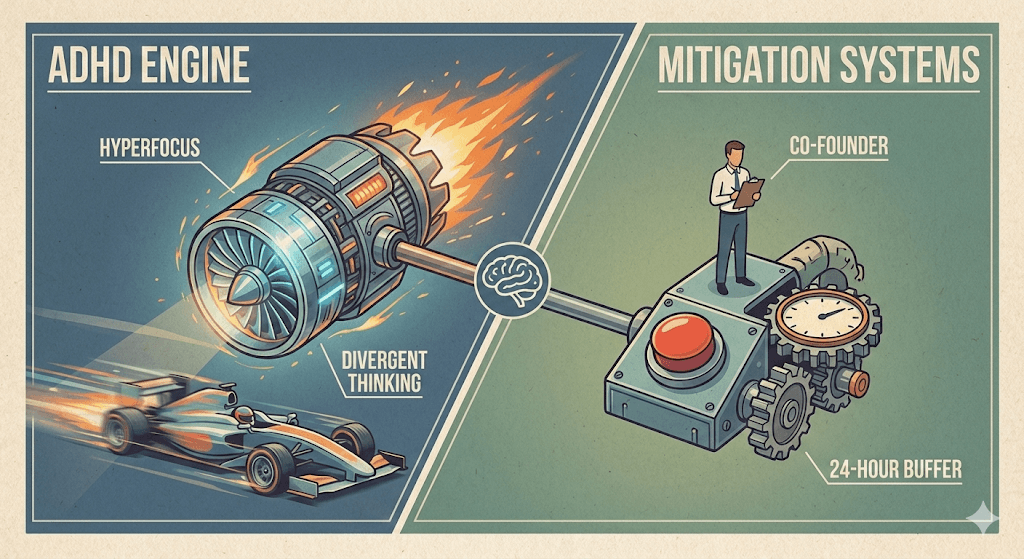

The Bicycle Brakes: Strategic Systemic Mitigation

The challenge with the ADHD profile is not the potential, but the lack of consistent operational scaffolding. The founder's greatest risks (impulsivity, time blindness, object permanence) are manageable with institutional-grade, pre-vetted systems. For the VC, this means investing in the System, not just the Founder.

Here are the three essential components of the risk mitigation playbook:

The Co-Founder Hedge (Alignment Check): The solo ADHD founder represents unmitigated risk. Investment should be contingent on a complementary co-founder structure (ideally 1-2 operators) who provide a stable operating rhythm. Their primary function is to serve as a high-friction "Say No" filter for impulse decisions and to manage the steady-state execution the ADHD brain naturally resists.

Founders Associate (The Executive Function Prosthetic): This role is a non-negotiable operational hire. The associate takes ownership of low-stimulation, high-detail tasks—bookkeeping, calendar management, deadline tracking, and administrative follow-through. They are the essential link between the founder's visionary "Now" and the necessary, but often ignored, "Not Now" of business operations.

The Mandatory 24-Hour Buffer: To mitigate the high-impact "impulse risk" often tied to hyperfocus, implement a mandated 24-hour cooling-off period. This rule must apply to critical, non-reversible decisions such as key hires, major budget allocations (big spends), or strategic pivots. This converts raw impulse into calculated risk.

The Tech Stack: From Pills to Platforms

The days of "just a pill" are over. While stimulants still dominate the ~$18.5B total market, accounting for over 60% share, we are seeing 18% CAGRs in Digital Therapeutics (DTx) and non-med tech and the “best practice” is more of a multi-modal play.

The Multi-Modal Play:

BCI & Neurofeedback: Companies like Neurable.com (which we're invested in) use brain-computer interfaces to help users "train" their focus.

DTx: The FDA has already cleared prescription video games (EndeavorRx) as legitimate treatment.

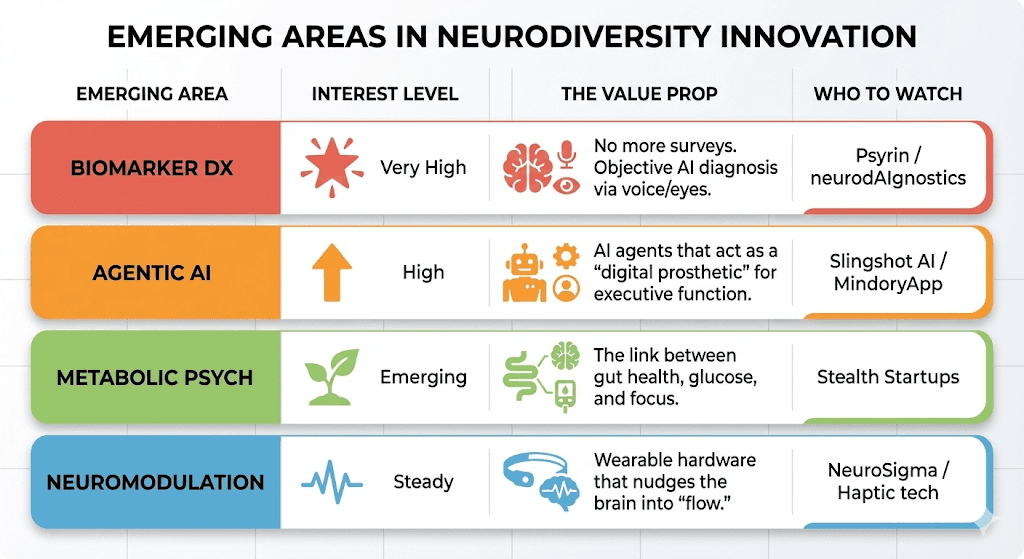

Where the Smart Money is Moving in 2026

The "Hype Cycle" trough is over. We've seen large raises, including Cerebral's $500M+ and Akili's significant SPAC-backed capitalization, followed by notable market corrections that sobered valuations across the sector. Now, the smart money is in the "Agentic AI" and Precision Biomarker Diagnostics phase.

The Bottom Line

The ADHD sector has matured. We aren't looking for the next stimulant anymore. We’re looking for the precision infrastructure that supports a neurodivergent world.

The era of institutional-grade, precision neuro-inclusion has arrived. The biggest returns won't come from "fixing" these brains—they'll come from the platforms that treat neurodiversity as the strategic asset it’s always been. The due diligence frontier is now the founder’s operating system.

Forget Silicon Valley's obsession with 'Genius.' The next wave of disruption is being built by the neurodivergent. With roughly 25-30% of self-employed founders meeting ADHD criteria, this article examines the complexities and the strategic investment opportunity presented by the high-performance ADHD cognitive profile.

The Breakdown: What are we actually talking about?

ADHD isn't just "being hyper." In 2026, we've moved past the deficit-only model. It's a double-edged sword — and it's important to name both edges honestly. For many people, ADHD is a genuine disability that causes significant daily impairment: lost jobs, strained relationships, and real suffering. At the same time, the same neurological profile that drives those challenges can also enable high-stakes crisis proficiency and divergent thinking that straight-line thinkers simply can't replicate.

We've been documenting this for 200 years, but only recently have we recognized there's no "blood test" for it. Diagnosis still relies on clinical evaluations of history and behavior. This diagnostic "bottleneck" is actually a significant investment opportunity — but to appreciate the scale, we must first understand the different components of the market.

The Market: By the Numbers (2026)

If you think ADHD is just a "kids' market," you’re missing the bigger opportunity. As of 2026, the sector is split into two massive, distinct opportunities:

The Pediatric Anchor: ~$12B. This is the bedrock of the sector, focused on ages 3-17.

The Adult Growth Engine: ~$7B. This is where the real "alpha" is for VC’s investing directly in ADHD solutions.

Why we think this is undervalued:

The C-Suite Disclosure: 44% of large orgs now have a senior exec who has publicly "come out" as neurodivergent. It’s becoming a corporate badge of honor.

The Founder Link: Roughly 25-30% of self-employed founders meet ADHD criteria.

Selection Bias: Fortune 500 leader traits: risk tolerance, high energy, and hyperfocus are ADHD traits. Think Richard Branson or JetBlue’s David Neeleman. These guys aren't outliers; they're the archetype.

Fact-Checking the Stereotypes

Forget the "kid who can’t sit still." In 2026, we look for the "Ferrari Engine (superpowers), Bicycle Brakes (systems or practical tools)" profile.

Here is the ground truth:

The Low Arousal Paradox: ADHD brains are actually under-stimulated. Stimulants (Adderall/Vyvanse) act like a "wake-up" signal so the brain can finally stop hunting for dopamine and just... focus.

Time Blindness: It’s not laziness; it’s Chronosagnosia. The brain perceives "Now" or "Not Now." This makes linear scheduling a nightmare, but makes them lethal in "sprint" environments.

Hyperfocus: The secret weapon. When the interest is there, the rest of the world (sleep, food, noise) vanishes.

The Gender Diagnostic Gap: Women and girls were missed for decades because they presented as "daydreamers" rather than "disruptive." This is a massive, underserved diagnostic market.

Ferrari Engine: The Superpowers (The Investment Thesis)

When you’re looking at a founder, you aren't looking for "normal." You're looking for these ADHD-driven edges:

Divergent Thinking: While most go A → B → C, these founders go A → Blue → Jazz → Space. That associative leap is where "disruption" actually comes from and directly leads to intellectual property that competitors, locked in linear thinking, cannot replicate or see.

Crisis Calm: Under-stimulated brains love chaos. When a startup faces an unexpected market shift, the ADHD founder is finally at their baseline and shows remarkable resilience by avoiding decision paralysis.

Pattern Recognition: They are "floodlights," not flashlights. They see the whole room (and the market shifts) at once.

The Bicycle Brakes: Strategic Systemic Mitigation

The challenge with the ADHD profile is not the potential, but the lack of consistent operational scaffolding. The founder's greatest risks (impulsivity, time blindness, object permanence) are manageable with institutional-grade, pre-vetted systems. For the VC, this means investing in the System, not just the Founder.

Here are the three essential components of the risk mitigation playbook:

The Co-Founder Hedge (Alignment Check): The solo ADHD founder represents unmitigated risk. Investment should be contingent on a complementary co-founder structure (ideally 1-2 operators) who provide a stable operating rhythm. Their primary function is to serve as a high-friction "Say No" filter for impulse decisions and to manage the steady-state execution the ADHD brain naturally resists.

Founders Associate (The Executive Function Prosthetic): This role is a non-negotiable operational hire. The associate takes ownership of low-stimulation, high-detail tasks—bookkeeping, calendar management, deadline tracking, and administrative follow-through. They are the essential link between the founder's visionary "Now" and the necessary, but often ignored, "Not Now" of business operations.

The Mandatory 24-Hour Buffer: To mitigate the high-impact "impulse risk" often tied to hyperfocus, implement a mandated 24-hour cooling-off period. This rule must apply to critical, non-reversible decisions such as key hires, major budget allocations (big spends), or strategic pivots. This converts raw impulse into calculated risk.

The Tech Stack: From Pills to Platforms

The days of "just a pill" are over. While stimulants still dominate the ~$18.5B total market, accounting for over 60% share, we are seeing 18% CAGRs in Digital Therapeutics (DTx) and non-med tech and the “best practice” is more of a multi-modal play.

The Multi-Modal Play:

BCI & Neurofeedback: Companies like Neurable.com (which we're invested in) use brain-computer interfaces to help users "train" their focus.

DTx: The FDA has already cleared prescription video games (EndeavorRx) as legitimate treatment.

Where the Smart Money is Moving in 2026

The "Hype Cycle" trough is over. We've seen large raises, including Cerebral's $500M+ and Akili's significant SPAC-backed capitalization, followed by notable market corrections that sobered valuations across the sector. Now, the smart money is in the "Agentic AI" and Precision Biomarker Diagnostics phase.

The Bottom Line

The ADHD sector has matured. We aren't looking for the next stimulant anymore. We’re looking for the precision infrastructure that supports a neurodivergent world.

The era of institutional-grade, precision neuro-inclusion has arrived. The biggest returns won't come from "fixing" these brains—they'll come from the platforms that treat neurodiversity as the strategic asset it’s always been. The due diligence frontier is now the founder’s operating system.

Forget Silicon Valley's obsession with 'Genius.' The next wave of disruption is being built by the neurodivergent. With roughly 25-30% of self-employed founders meeting ADHD criteria, this article examines the complexities and the strategic investment opportunity presented by the high-performance ADHD cognitive profile.

The Breakdown: What are we actually talking about?

ADHD isn't just "being hyper." In 2026, we've moved past the deficit-only model. It's a double-edged sword — and it's important to name both edges honestly. For many people, ADHD is a genuine disability that causes significant daily impairment: lost jobs, strained relationships, and real suffering. At the same time, the same neurological profile that drives those challenges can also enable high-stakes crisis proficiency and divergent thinking that straight-line thinkers simply can't replicate.

We've been documenting this for 200 years, but only recently have we recognized there's no "blood test" for it. Diagnosis still relies on clinical evaluations of history and behavior. This diagnostic "bottleneck" is actually a significant investment opportunity — but to appreciate the scale, we must first understand the different components of the market.

The Market: By the Numbers (2026)

If you think ADHD is just a "kids' market," you’re missing the bigger opportunity. As of 2026, the sector is split into two massive, distinct opportunities:

The Pediatric Anchor: ~$12B. This is the bedrock of the sector, focused on ages 3-17.

The Adult Growth Engine: ~$7B. This is where the real "alpha" is for VC’s investing directly in ADHD solutions.

Why we think this is undervalued:

The C-Suite Disclosure: 44% of large orgs now have a senior exec who has publicly "come out" as neurodivergent. It’s becoming a corporate badge of honor.

The Founder Link: Roughly 25-30% of self-employed founders meet ADHD criteria.

Selection Bias: Fortune 500 leader traits: risk tolerance, high energy, and hyperfocus are ADHD traits. Think Richard Branson or JetBlue’s David Neeleman. These guys aren't outliers; they're the archetype.

Fact-Checking the Stereotypes

Forget the "kid who can’t sit still." In 2026, we look for the "Ferrari Engine (superpowers), Bicycle Brakes (systems or practical tools)" profile.

Here is the ground truth:

The Low Arousal Paradox: ADHD brains are actually under-stimulated. Stimulants (Adderall/Vyvanse) act like a "wake-up" signal so the brain can finally stop hunting for dopamine and just... focus.

Time Blindness: It’s not laziness; it’s Chronosagnosia. The brain perceives "Now" or "Not Now." This makes linear scheduling a nightmare, but makes them lethal in "sprint" environments.

Hyperfocus: The secret weapon. When the interest is there, the rest of the world (sleep, food, noise) vanishes.

The Gender Diagnostic Gap: Women and girls were missed for decades because they presented as "daydreamers" rather than "disruptive." This is a massive, underserved diagnostic market.

Ferrari Engine: The Superpowers (The Investment Thesis)

When you’re looking at a founder, you aren't looking for "normal." You're looking for these ADHD-driven edges:

Divergent Thinking: While most go A → B → C, these founders go A → Blue → Jazz → Space. That associative leap is where "disruption" actually comes from and directly leads to intellectual property that competitors, locked in linear thinking, cannot replicate or see.

Crisis Calm: Under-stimulated brains love chaos. When a startup faces an unexpected market shift, the ADHD founder is finally at their baseline and shows remarkable resilience by avoiding decision paralysis.

Pattern Recognition: They are "floodlights," not flashlights. They see the whole room (and the market shifts) at once.

The Bicycle Brakes: Strategic Systemic Mitigation

The challenge with the ADHD profile is not the potential, but the lack of consistent operational scaffolding. The founder's greatest risks (impulsivity, time blindness, object permanence) are manageable with institutional-grade, pre-vetted systems. For the VC, this means investing in the System, not just the Founder.

Here are the three essential components of the risk mitigation playbook:

The Co-Founder Hedge (Alignment Check): The solo ADHD founder represents unmitigated risk. Investment should be contingent on a complementary co-founder structure (ideally 1-2 operators) who provide a stable operating rhythm. Their primary function is to serve as a high-friction "Say No" filter for impulse decisions and to manage the steady-state execution the ADHD brain naturally resists.

Founders Associate (The Executive Function Prosthetic): This role is a non-negotiable operational hire. The associate takes ownership of low-stimulation, high-detail tasks—bookkeeping, calendar management, deadline tracking, and administrative follow-through. They are the essential link between the founder's visionary "Now" and the necessary, but often ignored, "Not Now" of business operations.

The Mandatory 24-Hour Buffer: To mitigate the high-impact "impulse risk" often tied to hyperfocus, implement a mandated 24-hour cooling-off period. This rule must apply to critical, non-reversible decisions such as key hires, major budget allocations (big spends), or strategic pivots. This converts raw impulse into calculated risk.

The Tech Stack: From Pills to Platforms

The days of "just a pill" are over. While stimulants still dominate the ~$18.5B total market, accounting for over 60% share, we are seeing 18% CAGRs in Digital Therapeutics (DTx) and non-med tech and the “best practice” is more of a multi-modal play.

The Multi-Modal Play:

BCI & Neurofeedback: Companies like Neurable.com (which we're invested in) use brain-computer interfaces to help users "train" their focus.

DTx: The FDA has already cleared prescription video games (EndeavorRx) as legitimate treatment.

Where the Smart Money is Moving in 2026

The "Hype Cycle" trough is over. We've seen large raises, including Cerebral's $500M+ and Akili's significant SPAC-backed capitalization, followed by notable market corrections that sobered valuations across the sector. Now, the smart money is in the "Agentic AI" and Precision Biomarker Diagnostics phase.

The Bottom Line

The ADHD sector has matured. We aren't looking for the next stimulant anymore. We’re looking for the precision infrastructure that supports a neurodivergent world.

The era of institutional-grade, precision neuro-inclusion has arrived. The biggest returns won't come from "fixing" these brains—they'll come from the platforms that treat neurodiversity as the strategic asset it’s always been. The due diligence frontier is now the founder’s operating system.