The Agentic AI Boom: Inside Tech’s Next Big Race

The AI hype cycle has a new obsession: agents. Not chatbots, not copilots, but autonomous systems that can reason, act, and collaborate with minimal human input. Call them the next evolution of generative AI, or as some VCs now put it, “software that actually does stuff.”

07/11/2025

Marius Swart

And as it's always been with AI, the money (and the hype) is following fast.

According to Sifted, startups building AI agents have raised €5.2 billion in the first half of 2025, nearly double the total for all of 2024. Big Tech is piling in, too: OpenAI, Anthropic, Google, and Meta have all previewed “agentic” features meant to let their models handle multi-step tasks without babysitting.

From Copilots to Colleagues

At its core, agentic AI represents a shift from assistive systems to autonomous ones. The market now spans two worlds:

Digital agents, which exist purely in software: copilots, workflow bots, and digital assistants. They can be horizontal (cross-industry generalists) or vertical (specialists in areas like healthcare or finance).

Physical agents, which bridge digital and real space: autonomous vehicles, factory robots, and even medical devices that can adapt in real time.

Tech insiders describe the agentic maturity curve in four levels:

LLM-powered retrieval (basic copilots).

Single-task automation (task doers).

Cross-system orchestration (agents coordinating across tools).

Multi-agent constellations (agents supervising agents).

Most startups today sit somewhere between Levels 2 and 3, smart enough to execute complex workflows, but still too fragile for full autonomy. Level 4 remains a whiteboard dream.

The Gap Between Promise and Performance

Enterprise buyers love the idea of autonomous agents. The reality? Less magical.

The top three pain points cited by early adopters are:

Reliability - accuracy nosedives as complexity rises.

Integration headaches - agents don’t play nice with legacy stacks.

Lack of differentiation - too many horizontal clones chasing the same use cases.

“There’s still a big gap between what’s promised and what’s delivered,” one enterprise exec told TechCrunch. “The tech works great for simple tasks — but once you go deeper into workflows, you hit a wall.”

Data, Not Models, Is the Moat

As investors shift from model hype to data strategy, one truth stands out: your model is not your moat, your data is.

That’s why Meta’s surprise move to acquire a 49% stake in Scale AI, the data-labeling giant, sent shockwaves through the industry, prompting OpenAI and Google to cut ties. Scale dominates the data-labeling pipeline that shapes model performance, from basic thumbs-up feedback to full-blown human reinforcement training.

The problem? We are constrained in the amount of data available on the internet, as most players have used most of the training data possible. And this is ok for LLMs, but for more complex agents, like the physical AI ones, this represents a larger challenge (and hence why we feel teleoperation as a service will be around for a long time). Furthermore, models feast on massive web-scraped text, Reddit posts vastly outnumber academic papers, and subtle errors like sarcasm or bias leak straight into the outputs.

Synthetic Data and the Machines-Teaching-Machines Era

Enter synthetic data, AI-generated data used to train other AI systems. It’s cheaper, scalable, and already being used by leading models like China’s DeepSeek R1, which reportedly slashed training costs by relying heavily on synthetic datasets.

The new norm is hybrid: humans in the loop, but machines teaching machines. That blend is helping the industry move faster, but it’s not without risk. “There’s still no silver bullet,” the report notes. “Human oversight remains essential.”

Where the Smart Money Is Going

If you’re building on OpenAI’s API, beware: the moat is thin. The real opportunities lie in regulated verticals like life sciences/healthcare, finance, and energy, where proprietary data sets are protected and compliance creates high barriers to entry.

Combined, the Life Science and Healthcare industries are the fastest-growing data segments. The data sets are not only huge but also incredibly complex, requiring domain-specific agents doing actual operational work. Healthcare, in particular, is seeing a surge in AI agent adoption, from triaging medical data to integrating with HIPAA-compliant electronic health record systems. These aren’t chatbots; they’re domain-specific agents doing actual operational work.

As per this recent McKinsey article, there are several key use cases for agentic AI in the healthcare / life sciences sector.

These include:

Pharma Research – Accelerating Discovery and Deepening Scientific Insight. Companies like Owkin (France / US) and Causaly (UK)

Pharma Development – Accelerating Clinical Trials & Enhancing the Patient Journey (see details of “Why we invested in Bitfount” which helps life science stakeholders identify and recruit patients for clinical trials)

MedTech Research & Development – Accelerating Innovation and Prototyping.

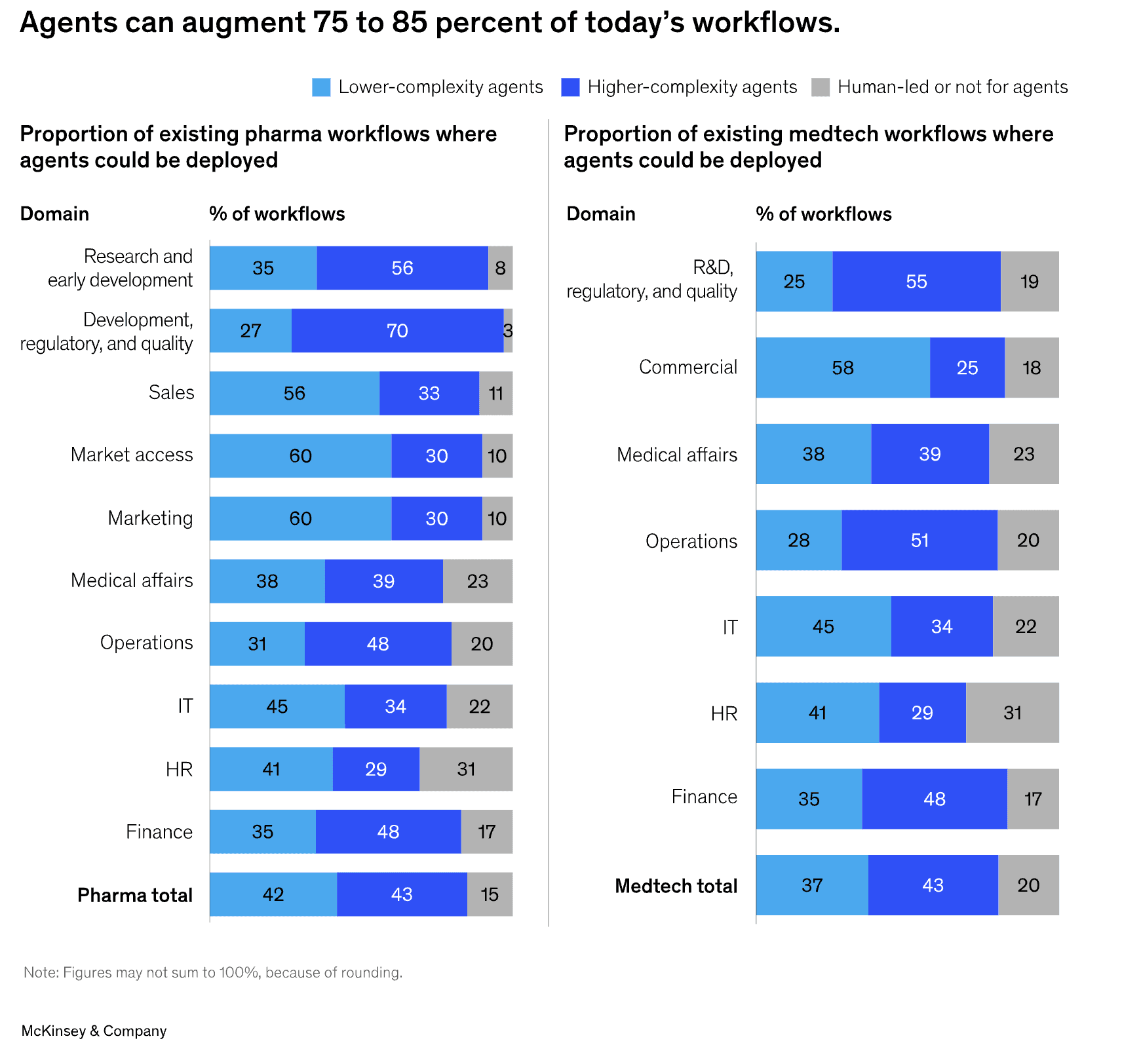

At Pace Ventures, we see the largest opportunities in commercial and operational workflows in pharma: 4 and 5 below. McKinsey estimated that Agentic AI could handle ~75-85% of current workflows, reducing task time in key areas (supply chain, procurement, manufacturing, quality) by ~25-35%.

This represents a massive TAM, and a few startups that come to mind are more established players like Axtria, but also earlier-stage companies like Semalytix (Germany) and Cellbyte (Germany).

Commercial (Pharma & MedTech) – Elevating Customer Engagement and Market Success.

Operations (Pharma & MedTech) – Accelerating Execution and Decision-Making

Information Technology – Transforming IT Operations and Driving Innovation

The SaaS Disruption Question

One of the biggest questions in venture circles right now:

Will agentic AI kill SaaS as we know it?

If agents can autonomously execute workflows, companies may stop paying per login or license. Instead, they’ll pay per outcome, for results, not seats. That could upend the business model that’s powered the software industry for two decades.

In three years, routine, rule-based tasks could move from “human + app” to “AI agent + API.”

That’s not just automation, it’s a re-architecture of how digital work gets done.

The Bottom Line

The race to build autonomous agents is only just beginning, but its impact could rival that of the mobile or cloud revolutions. For startups, the challenge is clear: the winners won’t just build smarter models, they’ll own cleaner data, deeper integrations, and defensible niches.

The age of agentic AI isn’t coming. It’s already here, and it’s hungry for your workflows.

And as it's always been with AI, the money (and the hype) is following fast.

According to Sifted, startups building AI agents have raised €5.2 billion in the first half of 2025, nearly double the total for all of 2024. Big Tech is piling in, too: OpenAI, Anthropic, Google, and Meta have all previewed “agentic” features meant to let their models handle multi-step tasks without babysitting.

From Copilots to Colleagues

At its core, agentic AI represents a shift from assistive systems to autonomous ones. The market now spans two worlds:

Digital agents, which exist purely in software: copilots, workflow bots, and digital assistants. They can be horizontal (cross-industry generalists) or vertical (specialists in areas like healthcare or finance).

Physical agents, which bridge digital and real space: autonomous vehicles, factory robots, and even medical devices that can adapt in real time.

Tech insiders describe the agentic maturity curve in four levels:

LLM-powered retrieval (basic copilots).

Single-task automation (task doers).

Cross-system orchestration (agents coordinating across tools).

Multi-agent constellations (agents supervising agents).

Most startups today sit somewhere between Levels 2 and 3, smart enough to execute complex workflows, but still too fragile for full autonomy. Level 4 remains a whiteboard dream.

The Gap Between Promise and Performance

Enterprise buyers love the idea of autonomous agents. The reality? Less magical.

The top three pain points cited by early adopters are:

Reliability - accuracy nosedives as complexity rises.

Integration headaches - agents don’t play nice with legacy stacks.

Lack of differentiation - too many horizontal clones chasing the same use cases.

“There’s still a big gap between what’s promised and what’s delivered,” one enterprise exec told TechCrunch. “The tech works great for simple tasks — but once you go deeper into workflows, you hit a wall.”

Data, Not Models, Is the Moat

As investors shift from model hype to data strategy, one truth stands out: your model is not your moat, your data is.

That’s why Meta’s surprise move to acquire a 49% stake in Scale AI, the data-labeling giant, sent shockwaves through the industry, prompting OpenAI and Google to cut ties. Scale dominates the data-labeling pipeline that shapes model performance, from basic thumbs-up feedback to full-blown human reinforcement training.

The problem? We are constrained in the amount of data available on the internet, as most players have used most of the training data possible. And this is ok for LLMs, but for more complex agents, like the physical AI ones, this represents a larger challenge (and hence why we feel teleoperation as a service will be around for a long time). Furthermore, models feast on massive web-scraped text, Reddit posts vastly outnumber academic papers, and subtle errors like sarcasm or bias leak straight into the outputs.

Synthetic Data and the Machines-Teaching-Machines Era

Enter synthetic data, AI-generated data used to train other AI systems. It’s cheaper, scalable, and already being used by leading models like China’s DeepSeek R1, which reportedly slashed training costs by relying heavily on synthetic datasets.

The new norm is hybrid: humans in the loop, but machines teaching machines. That blend is helping the industry move faster, but it’s not without risk. “There’s still no silver bullet,” the report notes. “Human oversight remains essential.”

Where the Smart Money Is Going

If you’re building on OpenAI’s API, beware: the moat is thin. The real opportunities lie in regulated verticals like life sciences/healthcare, finance, and energy, where proprietary data sets are protected and compliance creates high barriers to entry.

Combined, the Life Science and Healthcare industries are the fastest-growing data segments. The data sets are not only huge but also incredibly complex, requiring domain-specific agents doing actual operational work. Healthcare, in particular, is seeing a surge in AI agent adoption, from triaging medical data to integrating with HIPAA-compliant electronic health record systems. These aren’t chatbots; they’re domain-specific agents doing actual operational work.

As per this recent McKinsey article, there are several key use cases for agentic AI in the healthcare / life sciences sector.

These include:

Pharma Research – Accelerating Discovery and Deepening Scientific Insight. Companies like Owkin (France / US) and Causaly (UK)

Pharma Development – Accelerating Clinical Trials & Enhancing the Patient Journey (see details of “Why we invested in Bitfount” which helps life science stakeholders identify and recruit patients for clinical trials)

MedTech Research & Development – Accelerating Innovation and Prototyping.

At Pace Ventures, we see the largest opportunities in commercial and operational workflows in pharma: 4 and 5 below. McKinsey estimated that Agentic AI could handle ~75-85% of current workflows, reducing task time in key areas (supply chain, procurement, manufacturing, quality) by ~25-35%.

This represents a massive TAM, and a few startups that come to mind are more established players like Axtria, but also earlier-stage companies like Semalytix (Germany) and Cellbyte (Germany).

Commercial (Pharma & MedTech) – Elevating Customer Engagement and Market Success.

Operations (Pharma & MedTech) – Accelerating Execution and Decision-Making

Information Technology – Transforming IT Operations and Driving Innovation

The SaaS Disruption Question

One of the biggest questions in venture circles right now:

Will agentic AI kill SaaS as we know it?

If agents can autonomously execute workflows, companies may stop paying per login or license. Instead, they’ll pay per outcome, for results, not seats. That could upend the business model that’s powered the software industry for two decades.

In three years, routine, rule-based tasks could move from “human + app” to “AI agent + API.”

That’s not just automation, it’s a re-architecture of how digital work gets done.

The Bottom Line

The race to build autonomous agents is only just beginning, but its impact could rival that of the mobile or cloud revolutions. For startups, the challenge is clear: the winners won’t just build smarter models, they’ll own cleaner data, deeper integrations, and defensible niches.

The age of agentic AI isn’t coming. It’s already here, and it’s hungry for your workflows.

And as it's always been with AI, the money (and the hype) is following fast.

According to Sifted, startups building AI agents have raised €5.2 billion in the first half of 2025, nearly double the total for all of 2024. Big Tech is piling in, too: OpenAI, Anthropic, Google, and Meta have all previewed “agentic” features meant to let their models handle multi-step tasks without babysitting.

From Copilots to Colleagues

At its core, agentic AI represents a shift from assistive systems to autonomous ones. The market now spans two worlds:

Digital agents, which exist purely in software: copilots, workflow bots, and digital assistants. They can be horizontal (cross-industry generalists) or vertical (specialists in areas like healthcare or finance).

Physical agents, which bridge digital and real space: autonomous vehicles, factory robots, and even medical devices that can adapt in real time.

Tech insiders describe the agentic maturity curve in four levels:

LLM-powered retrieval (basic copilots).

Single-task automation (task doers).

Cross-system orchestration (agents coordinating across tools).

Multi-agent constellations (agents supervising agents).

Most startups today sit somewhere between Levels 2 and 3, smart enough to execute complex workflows, but still too fragile for full autonomy. Level 4 remains a whiteboard dream.

The Gap Between Promise and Performance

Enterprise buyers love the idea of autonomous agents. The reality? Less magical.

The top three pain points cited by early adopters are:

Reliability - accuracy nosedives as complexity rises.

Integration headaches - agents don’t play nice with legacy stacks.

Lack of differentiation - too many horizontal clones chasing the same use cases.

“There’s still a big gap between what’s promised and what’s delivered,” one enterprise exec told TechCrunch. “The tech works great for simple tasks — but once you go deeper into workflows, you hit a wall.”

Data, Not Models, Is the Moat

As investors shift from model hype to data strategy, one truth stands out: your model is not your moat, your data is.

That’s why Meta’s surprise move to acquire a 49% stake in Scale AI, the data-labeling giant, sent shockwaves through the industry, prompting OpenAI and Google to cut ties. Scale dominates the data-labeling pipeline that shapes model performance, from basic thumbs-up feedback to full-blown human reinforcement training.

The problem? We are constrained in the amount of data available on the internet, as most players have used most of the training data possible. And this is ok for LLMs, but for more complex agents, like the physical AI ones, this represents a larger challenge (and hence why we feel teleoperation as a service will be around for a long time). Furthermore, models feast on massive web-scraped text, Reddit posts vastly outnumber academic papers, and subtle errors like sarcasm or bias leak straight into the outputs.

Synthetic Data and the Machines-Teaching-Machines Era

Enter synthetic data, AI-generated data used to train other AI systems. It’s cheaper, scalable, and already being used by leading models like China’s DeepSeek R1, which reportedly slashed training costs by relying heavily on synthetic datasets.

The new norm is hybrid: humans in the loop, but machines teaching machines. That blend is helping the industry move faster, but it’s not without risk. “There’s still no silver bullet,” the report notes. “Human oversight remains essential.”

Where the Smart Money Is Going

If you’re building on OpenAI’s API, beware: the moat is thin. The real opportunities lie in regulated verticals like life sciences/healthcare, finance, and energy, where proprietary data sets are protected and compliance creates high barriers to entry.

Combined, the Life Science and Healthcare industries are the fastest-growing data segments. The data sets are not only huge but also incredibly complex, requiring domain-specific agents doing actual operational work. Healthcare, in particular, is seeing a surge in AI agent adoption, from triaging medical data to integrating with HIPAA-compliant electronic health record systems. These aren’t chatbots; they’re domain-specific agents doing actual operational work.

As per this recent McKinsey article, there are several key use cases for agentic AI in the healthcare / life sciences sector.

These include:

Pharma Research – Accelerating Discovery and Deepening Scientific Insight. Companies like Owkin (France / US) and Causaly (UK)

Pharma Development – Accelerating Clinical Trials & Enhancing the Patient Journey (see details of “Why we invested in Bitfount” which helps life science stakeholders identify and recruit patients for clinical trials)

MedTech Research & Development – Accelerating Innovation and Prototyping.

At Pace Ventures, we see the largest opportunities in commercial and operational workflows in pharma: 4 and 5 below. McKinsey estimated that Agentic AI could handle ~75-85% of current workflows, reducing task time in key areas (supply chain, procurement, manufacturing, quality) by ~25-35%.

This represents a massive TAM, and a few startups that come to mind are more established players like Axtria, but also earlier-stage companies like Semalytix (Germany) and Cellbyte (Germany).

Commercial (Pharma & MedTech) – Elevating Customer Engagement and Market Success.

Operations (Pharma & MedTech) – Accelerating Execution and Decision-Making

Information Technology – Transforming IT Operations and Driving Innovation

The SaaS Disruption Question

One of the biggest questions in venture circles right now:

Will agentic AI kill SaaS as we know it?

If agents can autonomously execute workflows, companies may stop paying per login or license. Instead, they’ll pay per outcome, for results, not seats. That could upend the business model that’s powered the software industry for two decades.

In three years, routine, rule-based tasks could move from “human + app” to “AI agent + API.”

That’s not just automation, it’s a re-architecture of how digital work gets done.

The Bottom Line

The race to build autonomous agents is only just beginning, but its impact could rival that of the mobile or cloud revolutions. For startups, the challenge is clear: the winners won’t just build smarter models, they’ll own cleaner data, deeper integrations, and defensible niches.

The age of agentic AI isn’t coming. It’s already here, and it’s hungry for your workflows.