Let’s Talk About Digital Mental Health

The importance of mental health is currently more discussed than ever before. Since the start of the global pandemic in 2020, anxiety and depression have exponentially increased and, in some countries, even doubled.

Katharina Neisinger

The importance of mental health is currently more discussed than ever before. Since the start of the global pandemic in 2020, anxiety and depression have exponentially increased and, in some countries, even doubled (1) and 1 in 5 people have reported feeling anxious or depressed in the last few months (2).

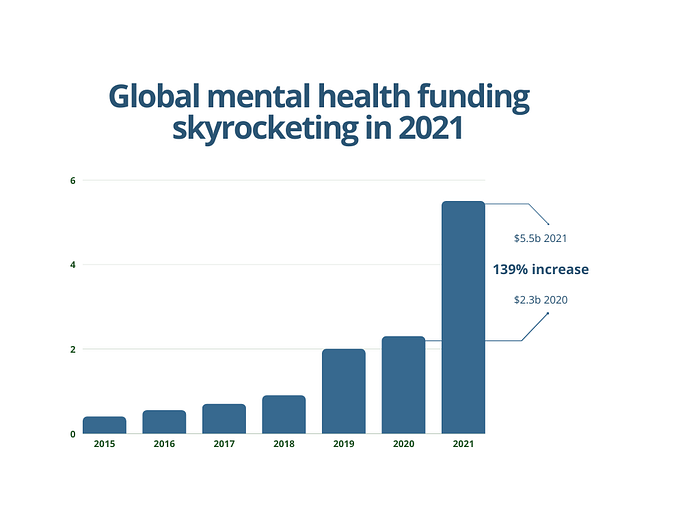

It is therefore not surprising to see that global deals into mental health start-ups reached new highs in 2021. Total investments in the sector in 2021 is estimated to have reached $5.5B, a 139% YoY increase from 2020 (3).

Global mental health funding skyrocketing in 2021 (2)

From a regional point of view, U.S. mental health companies continued to see the most robust inflow of funding with $4.5 billion, or 82% of the total, in funding last year. European start-ups raised $651 million, and Asian companies raised $289 million. While these are significant numbers, almost 68% of the deals in 2021 were early-stage, implying there is still plenty of room for growth (2).

The significant investment level and continued discussion on social media on the importance of mental health, has helped to partially lift the stigma commonly associated with mental health conditions. It has also resulted in even more offerings, with both employers and consumers today having several options to choose from to support with early diagnosis and/or teletherapy solutions. However, an increase in providers doesn’t necessarily cater to a global diverse audience; specific demographics and needs are still underserved, with many either not receiving treatment or undertreated.

Especially children and adolescents, who have been the most affected by “learning from home” and other isolation policies during Covid-19, have often not received adequate support. And the numbers are staggering; major depression among teens in the U.S., especially girls, has jumped by 37% in the last decade. Furthermore, more than three million adolescents aged 12–17 reported at least one major depressive episode in the recent past (4).

Given the numbers referenced above, we feel the need to talk in more detail about the digital mental health space.

Mapping out the playing field

Mental health approaches are segmented into prevention, diagnostic, and treatment areas.

Before the pandemic, a lot has happened in the prevention space: apps such as Calm (est. 2012 US, $191.25m total funding) and Headspace (est. 2010 US, $215.65m total funding) created awareness to improve one’s general health through mindfulness and meditation. The early success of these companies resulted in other start-ups incorporating similar themes into their business model. Today, guided meditations, breathing exercises, and journaling pop up frequently.

Then there are companies targeting more specific problem areas, such as anxiety, sleep, and motivation. These are MostDays (est. 2020 US, $3.20m total funding), MindLabs (est. 2020 UK, $5.23m total funding), or Mindshine (est. 2018 Germany).

Mapping out the digital mental health space

On the diagnostic end, many digital mental health treatment providers inherently act as a diagnostic tool as well. Yet, we feel that with digital mental health solutions, the opportunity for misdiagnosis is higher. A simple questionnaire, which many start-ups use as their user-assessment tool, can’t capture certain vital traits to ensure the proper treatment.

Thymia.ai (est. 2020 UK, $2.6m total funding), for example, has developed an interesting biometric approach to diagnosing depression and related disorders. They use video games to collect voice and facial expressions of patients, signaling when they are exhibiting symptoms linked to the behavioral patterns of someone with depression. Another exciting start-up is Alena (est. 2019 UK, $2.8m total funding), which uses neuroscience-based assessments, in the form of playing simple games, to assess how your brain works and then provide users with behavioral therapy to overcome social anxiety.

Turning our focus to treatment, we see a lot of teletherapy plays. There are full-stack approaches such as TalkSpace (est. 2011 US, $413.7m total funding) covering therapy for individuals, couples, teens, and within psychiatry also offer a medication management plan. They operate as both a B2B and D2C business but their D2C approach appears to have numerous difficulties with their conversion and retention, which tends to drive high marketing spending (5). Contrastingly, Koa Health (est. 2016 UK, $36.32m total funding) is also tackling the therapeutic and diagnostic segments but operates exclusively as reimbursable B2B. Therefore, based on our evaluation of B2B vs. D2C, we concluded the economics of D2C appear super tricky, and hence we prefer either the B2B or B2B2C business models.

“Mental health is not a destination, but a process”

Another segment in the therapeutic space that has been getting a lot of attention, albeit not always positive, is prescribed digital mental health: see HelloBetter (est. 2015 Germany, $12m total funding), offering stress and burnout courses that prescribed by doctors and therapists (reimbursable B2C/B2B2C approach). Digital therapy solutions are now reimbursable due to the introduction of DiGA in Germany (digital health applications, “Digital Gesundheitsanwendungen”): a DiGA is a CE-marked medical device. (It seems very likely that France and several other European countries will also allow for reimbursement of digital solutions in the future)

Some physicians we spoke with say that even with the DiGA “approval stamp” adoption rates will not pick up immediately as a) the system and doctors are not adequately trained on how to operate the DiGA environment, and b) it excludes a big target audience that would love to use a vetted product but do not want to go the extra step to go to the doctor’s office for a prescription.

We have seen virtual care platforms in the domains described above expanding horizontally and vertically within clinical fields. For example, Headspace (B2C) acquired Ginger (est. 2011 US $236m total funding) (B2B) for $3b in a vertical integration play, aiming to become a leading provider of digital behavioral health. Together, Ginger and Headspace will reach 100 million consumers. In turn, K Health (est. 2016 US, $278m total funding), a telehealth primary care provider, acquired Trusst (est. 2019 US), a messaging-based mental health platform, in a horizontal manner (B2C).

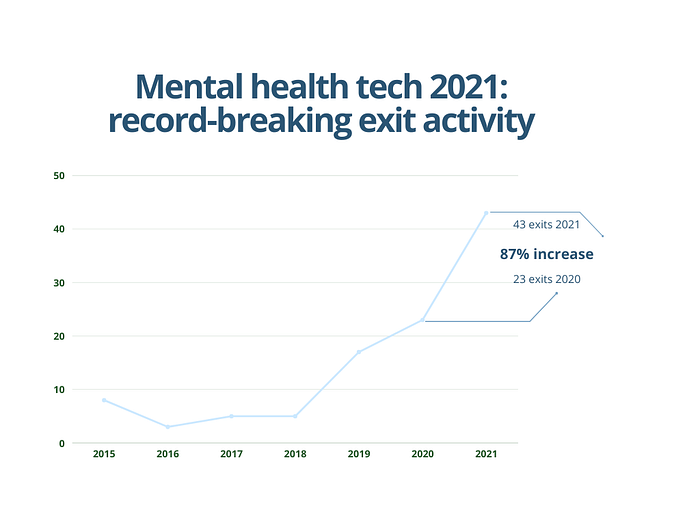

Record-breaking exit activity largely driven by M&A deals (2)

As can be seen from the chart above, 2021 was already a banner year for M&A exits, with 43 exits on record, an 87% increase over 2020, and we expect this trend to continue in the next 12 to 24 months given the high number of players and how fragmented the market has become (3).

Our belief is in the end, only a few players will be able to capture a large share of the overall mental health market. The success of those companies will depend on several factors: their level of scientific backing and the breadth of offerings they can provide (in this case, the direct or indirect communication to psychotherapists), and a seamless user experience.

Mental health for employees

A particular segment of digital mental health getting a lot of attention focuses on the workforce. Overall, four in ten US employees reported that their mental health declined due to the pandemic (6). No surprise then that 76% of U.S. employers increased investments into virtual care offering (7). For example, the U.S.-based Spring Health (est. 2016, $297.49m total funding) take a very data-driven approach to personalize their support for teams (from subclinical preventative to clinical treatment solutions).

In Europe: Nilo.Health (est. 2019 Germany), and Kyan Health (est. 2021 Switzerland, $1.67m total funding) cover a full-stack mental health offering for employees: from bite-sized auditory content to journaling and professional counseling services. Moka.Care (est. 2020 France, $18M total funding) place more emphasis on group therapy sessions.

From our research, we have two main observations regarding mental health for the workforce: firstly, many start-ups focus on the individual only. However, we believe that a combination of standard care for both teams and personalized tools for individuals is the best way forward. Secondly, virtual care platforms will succeed by adopting a holistic health-partnership strategy.

Younger generations

Maintaining good mental health over the last two years has been challenging, but seeking help has, for adults at least, has never been easier given the breadth of options as outlined above. Yet, younger generations, particularly children who may have suffered the most from the lack of vital social environments, do not find such a broad range of offerings, especially not in Europe. Studies show that digital mental health interventions (DMHIs) for the younger population can increase “efficiency, reach, and standardization as well as reduce costs of providing of mental health care” (8).

Coincidentally, an article by Fortune states that kids say their mental health is fine; but experts disagree (9). Kids’ self-reported responses to a survey show that of the over 1,000 kids and teens, 89% described their mental health as very good or somewhat good, and 80% said they are a little or not at all concerned about their mental health. Mental health professionals view this data as part of a multilayered and complex story, whereby there is a tendency for some kids to underreport mental health struggles, with the limited availability of mental health care feeding into this trend.

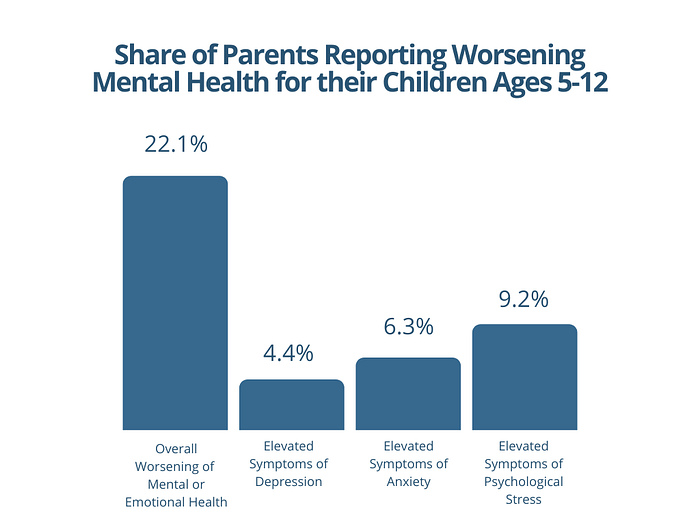

Children’s Worsening Mental Health due to Pandemic (November 2020) (10)

Some of the previously-mentioned companies in this article also target families and kids, such as subsections of Talkspace or Calm. Yet, we feel that the younger generation’s needs are vastly different from adults’ and should therefore be treated differently. For example, US Gen Z employees saw the highest percentage of declining mental health in 2021; in contrast, this was lowest among Boomers. Many Gen Z-ers were in the midst of one of their most defining chapters of life, studying at university or just having graduated and finding a completely different set-up of working environments. That is why we are excited by specialized mental health approaches such as Uwill, an online therapy platform explicitly targeting college students (est. 2020 US, $8.5m total funding).

As it relates to the content, many companies focus on sleep and relaxation tools only, and indeed there has been a massive influx of preventative mental health apps on the market. To help build trust with parents, our advice is that even preventative apps, need to conduct studies on their efficacy and leverage their pedagogical value. Trust will ultimately be the deciding factor to drive WOM user adoption, reducing the need for significant marketing spend on performance marketing or micro-influencers, the impact of which we have seen to decline over time as the company scales.

Nuances in start-up offerings for children are also important. For example, we love what Aumio (est. 2019 Germany) is doing with their content, walking kids through one coherent storyline to enable better identification with states of mind. Another prominent player is Moshi (est. 2017 UK, $23m total funding), which combines entertainment and mindfulness and has seen very good traction in the U.S. Both start-ups are highly-rated and provide a good gateway into the mental health space for young children.

Although both players are blending elements of mindfulness and entertainment, we see Moshi rather on the entertainment side and Aumio on the mindfulness end of the spectrum. Both players are thus able to capture a broad audience, but parents will need to assess what type of content their children need.

Parents will need to carefully assess DMHIs for their children

We see an unmet need targeting children on the therapeutic and diagnostic side, with only a few notable incumbents. Probably, the two most well-known are Little Otter (est. 2019 US, $26.2m total funding) and Daybreak Health (est. 2020 US, $12m total funding). Little Otter covers both the toddler to adolescent age group and the entire family, all through a very easy-to-navigate online therapy solution. Daybreak Health realized that 80% of teens with mental health needs were untreated. They partner with youth, families, and schools to create personalized, easily accessible, and affordable mental health programs by matching children with a licensed clinician.

Similar to companies targeting the workplace, DMHIs for children should target schools and educational settings to identify those experiencing or at risk of developing psychological symptoms (11). We think it is crucial to include DMHIs even without a present problem, and we would love to see it become part of school curricula. That way, we feel children will better understand what emotions or states of mind they are experiencing and can more easily identify and act on these when they arise.

Many parents struggle with their children’s mental health issues but do not know where to turn for help. Luckily, the rise of digital offerings present an opportunity to educate our children about mental health.

In summary, mental health conditions are increasing worldwide. Mental health conditions have a substantial effect on all areas of life, and WHO estimates that two of the most common mental health conditions, depression, and anxiety, cost the global economy around US$1 trillion each year. Despite these figures, global government-sponsored programs targeting mental health are less than 2% (12). It is no wonder the private sector has stepped up and we are excited to see what lies ahead.

If you know any companies targeting adolescent mental health, feel free to get in touch with us.

Published March 2022; updated August 2022.

Sources

OECD. Tackling the mental health impact of the COVID-19 crisis: An integrated, whole-of-society response. May 2021.

BBC. Depression doubles during Coronavirus. August 2020.

CB Insights. State of Mental Health Tech 2021 Report. February 2022.

Time. Insurance Claim Data Show How Much Teen Mental Health Has Suffered During the U.S. COVID-19 Pandemic. March 2021. / Time. Depression and Suicide Rates are rising sharply…

Global News Wire. Talkspace, Inc. Investors with Substantial Losses Have Opportunity to Lead Class Action Lawsuit. March 2022.

Statista. Employee Mental Health Changes Covid 19 by generation. August 2021.

Business Group on Health. Health Equity, Impact of Pandemic Among Large Employers’ Top Concerns. August 2021.

Cognitive and Behavioral Practice. Khanna, M.S., and Carper, M. Digital Mental Health Interventions for Child and Adolescent Anxiety. February 2022.

Fortune. Kids say their mental health is fine. Experts disagree. December 2021.

KKF. Mental Health and Substance Use Considerations Among Children During the COVID-19 Pandemic. May 2021.

Davies, S.M., et al. Preventative Digital Mental Health for Children in Primary Schools: Acceptability and Feasibility Study. December 2021.

World Health Organization. Mental Health. November 2021.

The importance of mental health is currently more discussed than ever before. Since the start of the global pandemic in 2020, anxiety and depression have exponentially increased and, in some countries, even doubled (1) and 1 in 5 people have reported feeling anxious or depressed in the last few months (2).

It is therefore not surprising to see that global deals into mental health start-ups reached new highs in 2021. Total investments in the sector in 2021 is estimated to have reached $5.5B, a 139% YoY increase from 2020 (3).

Global mental health funding skyrocketing in 2021 (2)

From a regional point of view, U.S. mental health companies continued to see the most robust inflow of funding with $4.5 billion, or 82% of the total, in funding last year. European start-ups raised $651 million, and Asian companies raised $289 million. While these are significant numbers, almost 68% of the deals in 2021 were early-stage, implying there is still plenty of room for growth (2).

The significant investment level and continued discussion on social media on the importance of mental health, has helped to partially lift the stigma commonly associated with mental health conditions. It has also resulted in even more offerings, with both employers and consumers today having several options to choose from to support with early diagnosis and/or teletherapy solutions. However, an increase in providers doesn’t necessarily cater to a global diverse audience; specific demographics and needs are still underserved, with many either not receiving treatment or undertreated.

Especially children and adolescents, who have been the most affected by “learning from home” and other isolation policies during Covid-19, have often not received adequate support. And the numbers are staggering; major depression among teens in the U.S., especially girls, has jumped by 37% in the last decade. Furthermore, more than three million adolescents aged 12–17 reported at least one major depressive episode in the recent past (4).

Given the numbers referenced above, we feel the need to talk in more detail about the digital mental health space.

Mapping out the playing field

Mental health approaches are segmented into prevention, diagnostic, and treatment areas.

Before the pandemic, a lot has happened in the prevention space: apps such as Calm (est. 2012 US, $191.25m total funding) and Headspace (est. 2010 US, $215.65m total funding) created awareness to improve one’s general health through mindfulness and meditation. The early success of these companies resulted in other start-ups incorporating similar themes into their business model. Today, guided meditations, breathing exercises, and journaling pop up frequently.

Then there are companies targeting more specific problem areas, such as anxiety, sleep, and motivation. These are MostDays (est. 2020 US, $3.20m total funding), MindLabs (est. 2020 UK, $5.23m total funding), or Mindshine (est. 2018 Germany).

Mapping out the digital mental health space

On the diagnostic end, many digital mental health treatment providers inherently act as a diagnostic tool as well. Yet, we feel that with digital mental health solutions, the opportunity for misdiagnosis is higher. A simple questionnaire, which many start-ups use as their user-assessment tool, can’t capture certain vital traits to ensure the proper treatment.

Thymia.ai (est. 2020 UK, $2.6m total funding), for example, has developed an interesting biometric approach to diagnosing depression and related disorders. They use video games to collect voice and facial expressions of patients, signaling when they are exhibiting symptoms linked to the behavioral patterns of someone with depression. Another exciting start-up is Alena (est. 2019 UK, $2.8m total funding), which uses neuroscience-based assessments, in the form of playing simple games, to assess how your brain works and then provide users with behavioral therapy to overcome social anxiety.

Turning our focus to treatment, we see a lot of teletherapy plays. There are full-stack approaches such as TalkSpace (est. 2011 US, $413.7m total funding) covering therapy for individuals, couples, teens, and within psychiatry also offer a medication management plan. They operate as both a B2B and D2C business but their D2C approach appears to have numerous difficulties with their conversion and retention, which tends to drive high marketing spending (5). Contrastingly, Koa Health (est. 2016 UK, $36.32m total funding) is also tackling the therapeutic and diagnostic segments but operates exclusively as reimbursable B2B. Therefore, based on our evaluation of B2B vs. D2C, we concluded the economics of D2C appear super tricky, and hence we prefer either the B2B or B2B2C business models.

“Mental health is not a destination, but a process”

Another segment in the therapeutic space that has been getting a lot of attention, albeit not always positive, is prescribed digital mental health: see HelloBetter (est. 2015 Germany, $12m total funding), offering stress and burnout courses that prescribed by doctors and therapists (reimbursable B2C/B2B2C approach). Digital therapy solutions are now reimbursable due to the introduction of DiGA in Germany (digital health applications, “Digital Gesundheitsanwendungen”): a DiGA is a CE-marked medical device. (It seems very likely that France and several other European countries will also allow for reimbursement of digital solutions in the future)

Some physicians we spoke with say that even with the DiGA “approval stamp” adoption rates will not pick up immediately as a) the system and doctors are not adequately trained on how to operate the DiGA environment, and b) it excludes a big target audience that would love to use a vetted product but do not want to go the extra step to go to the doctor’s office for a prescription.

We have seen virtual care platforms in the domains described above expanding horizontally and vertically within clinical fields. For example, Headspace (B2C) acquired Ginger (est. 2011 US $236m total funding) (B2B) for $3b in a vertical integration play, aiming to become a leading provider of digital behavioral health. Together, Ginger and Headspace will reach 100 million consumers. In turn, K Health (est. 2016 US, $278m total funding), a telehealth primary care provider, acquired Trusst (est. 2019 US), a messaging-based mental health platform, in a horizontal manner (B2C).

Record-breaking exit activity largely driven by M&A deals (2)

As can be seen from the chart above, 2021 was already a banner year for M&A exits, with 43 exits on record, an 87% increase over 2020, and we expect this trend to continue in the next 12 to 24 months given the high number of players and how fragmented the market has become (3).

Our belief is in the end, only a few players will be able to capture a large share of the overall mental health market. The success of those companies will depend on several factors: their level of scientific backing and the breadth of offerings they can provide (in this case, the direct or indirect communication to psychotherapists), and a seamless user experience.

Mental health for employees

A particular segment of digital mental health getting a lot of attention focuses on the workforce. Overall, four in ten US employees reported that their mental health declined due to the pandemic (6). No surprise then that 76% of U.S. employers increased investments into virtual care offering (7). For example, the U.S.-based Spring Health (est. 2016, $297.49m total funding) take a very data-driven approach to personalize their support for teams (from subclinical preventative to clinical treatment solutions).

In Europe: Nilo.Health (est. 2019 Germany), and Kyan Health (est. 2021 Switzerland, $1.67m total funding) cover a full-stack mental health offering for employees: from bite-sized auditory content to journaling and professional counseling services. Moka.Care (est. 2020 France, $18M total funding) place more emphasis on group therapy sessions.

From our research, we have two main observations regarding mental health for the workforce: firstly, many start-ups focus on the individual only. However, we believe that a combination of standard care for both teams and personalized tools for individuals is the best way forward. Secondly, virtual care platforms will succeed by adopting a holistic health-partnership strategy.

Younger generations

Maintaining good mental health over the last two years has been challenging, but seeking help has, for adults at least, has never been easier given the breadth of options as outlined above. Yet, younger generations, particularly children who may have suffered the most from the lack of vital social environments, do not find such a broad range of offerings, especially not in Europe. Studies show that digital mental health interventions (DMHIs) for the younger population can increase “efficiency, reach, and standardization as well as reduce costs of providing of mental health care” (8).

Coincidentally, an article by Fortune states that kids say their mental health is fine; but experts disagree (9). Kids’ self-reported responses to a survey show that of the over 1,000 kids and teens, 89% described their mental health as very good or somewhat good, and 80% said they are a little or not at all concerned about their mental health. Mental health professionals view this data as part of a multilayered and complex story, whereby there is a tendency for some kids to underreport mental health struggles, with the limited availability of mental health care feeding into this trend.

Children’s Worsening Mental Health due to Pandemic (November 2020) (10)

Some of the previously-mentioned companies in this article also target families and kids, such as subsections of Talkspace or Calm. Yet, we feel that the younger generation’s needs are vastly different from adults’ and should therefore be treated differently. For example, US Gen Z employees saw the highest percentage of declining mental health in 2021; in contrast, this was lowest among Boomers. Many Gen Z-ers were in the midst of one of their most defining chapters of life, studying at university or just having graduated and finding a completely different set-up of working environments. That is why we are excited by specialized mental health approaches such as Uwill, an online therapy platform explicitly targeting college students (est. 2020 US, $8.5m total funding).

As it relates to the content, many companies focus on sleep and relaxation tools only, and indeed there has been a massive influx of preventative mental health apps on the market. To help build trust with parents, our advice is that even preventative apps, need to conduct studies on their efficacy and leverage their pedagogical value. Trust will ultimately be the deciding factor to drive WOM user adoption, reducing the need for significant marketing spend on performance marketing or micro-influencers, the impact of which we have seen to decline over time as the company scales.

Nuances in start-up offerings for children are also important. For example, we love what Aumio (est. 2019 Germany) is doing with their content, walking kids through one coherent storyline to enable better identification with states of mind. Another prominent player is Moshi (est. 2017 UK, $23m total funding), which combines entertainment and mindfulness and has seen very good traction in the U.S. Both start-ups are highly-rated and provide a good gateway into the mental health space for young children.

Although both players are blending elements of mindfulness and entertainment, we see Moshi rather on the entertainment side and Aumio on the mindfulness end of the spectrum. Both players are thus able to capture a broad audience, but parents will need to assess what type of content their children need.

Parents will need to carefully assess DMHIs for their children

We see an unmet need targeting children on the therapeutic and diagnostic side, with only a few notable incumbents. Probably, the two most well-known are Little Otter (est. 2019 US, $26.2m total funding) and Daybreak Health (est. 2020 US, $12m total funding). Little Otter covers both the toddler to adolescent age group and the entire family, all through a very easy-to-navigate online therapy solution. Daybreak Health realized that 80% of teens with mental health needs were untreated. They partner with youth, families, and schools to create personalized, easily accessible, and affordable mental health programs by matching children with a licensed clinician.

Similar to companies targeting the workplace, DMHIs for children should target schools and educational settings to identify those experiencing or at risk of developing psychological symptoms (11). We think it is crucial to include DMHIs even without a present problem, and we would love to see it become part of school curricula. That way, we feel children will better understand what emotions or states of mind they are experiencing and can more easily identify and act on these when they arise.

Many parents struggle with their children’s mental health issues but do not know where to turn for help. Luckily, the rise of digital offerings present an opportunity to educate our children about mental health.

In summary, mental health conditions are increasing worldwide. Mental health conditions have a substantial effect on all areas of life, and WHO estimates that two of the most common mental health conditions, depression, and anxiety, cost the global economy around US$1 trillion each year. Despite these figures, global government-sponsored programs targeting mental health are less than 2% (12). It is no wonder the private sector has stepped up and we are excited to see what lies ahead.

If you know any companies targeting adolescent mental health, feel free to get in touch with us.

Published March 2022; updated August 2022.

Sources

OECD. Tackling the mental health impact of the COVID-19 crisis: An integrated, whole-of-society response. May 2021.

BBC. Depression doubles during Coronavirus. August 2020.

CB Insights. State of Mental Health Tech 2021 Report. February 2022.

Time. Insurance Claim Data Show How Much Teen Mental Health Has Suffered During the U.S. COVID-19 Pandemic. March 2021. / Time. Depression and Suicide Rates are rising sharply…

Global News Wire. Talkspace, Inc. Investors with Substantial Losses Have Opportunity to Lead Class Action Lawsuit. March 2022.

Statista. Employee Mental Health Changes Covid 19 by generation. August 2021.

Business Group on Health. Health Equity, Impact of Pandemic Among Large Employers’ Top Concerns. August 2021.

Cognitive and Behavioral Practice. Khanna, M.S., and Carper, M. Digital Mental Health Interventions for Child and Adolescent Anxiety. February 2022.

Fortune. Kids say their mental health is fine. Experts disagree. December 2021.

KKF. Mental Health and Substance Use Considerations Among Children During the COVID-19 Pandemic. May 2021.

Davies, S.M., et al. Preventative Digital Mental Health for Children in Primary Schools: Acceptability and Feasibility Study. December 2021.

World Health Organization. Mental Health. November 2021.

The importance of mental health is currently more discussed than ever before. Since the start of the global pandemic in 2020, anxiety and depression have exponentially increased and, in some countries, even doubled (1) and 1 in 5 people have reported feeling anxious or depressed in the last few months (2).

It is therefore not surprising to see that global deals into mental health start-ups reached new highs in 2021. Total investments in the sector in 2021 is estimated to have reached $5.5B, a 139% YoY increase from 2020 (3).

Global mental health funding skyrocketing in 2021 (2)

From a regional point of view, U.S. mental health companies continued to see the most robust inflow of funding with $4.5 billion, or 82% of the total, in funding last year. European start-ups raised $651 million, and Asian companies raised $289 million. While these are significant numbers, almost 68% of the deals in 2021 were early-stage, implying there is still plenty of room for growth (2).

The significant investment level and continued discussion on social media on the importance of mental health, has helped to partially lift the stigma commonly associated with mental health conditions. It has also resulted in even more offerings, with both employers and consumers today having several options to choose from to support with early diagnosis and/or teletherapy solutions. However, an increase in providers doesn’t necessarily cater to a global diverse audience; specific demographics and needs are still underserved, with many either not receiving treatment or undertreated.

Especially children and adolescents, who have been the most affected by “learning from home” and other isolation policies during Covid-19, have often not received adequate support. And the numbers are staggering; major depression among teens in the U.S., especially girls, has jumped by 37% in the last decade. Furthermore, more than three million adolescents aged 12–17 reported at least one major depressive episode in the recent past (4).

Given the numbers referenced above, we feel the need to talk in more detail about the digital mental health space.

Mapping out the playing field

Mental health approaches are segmented into prevention, diagnostic, and treatment areas.

Before the pandemic, a lot has happened in the prevention space: apps such as Calm (est. 2012 US, $191.25m total funding) and Headspace (est. 2010 US, $215.65m total funding) created awareness to improve one’s general health through mindfulness and meditation. The early success of these companies resulted in other start-ups incorporating similar themes into their business model. Today, guided meditations, breathing exercises, and journaling pop up frequently.

Then there are companies targeting more specific problem areas, such as anxiety, sleep, and motivation. These are MostDays (est. 2020 US, $3.20m total funding), MindLabs (est. 2020 UK, $5.23m total funding), or Mindshine (est. 2018 Germany).

Mapping out the digital mental health space

On the diagnostic end, many digital mental health treatment providers inherently act as a diagnostic tool as well. Yet, we feel that with digital mental health solutions, the opportunity for misdiagnosis is higher. A simple questionnaire, which many start-ups use as their user-assessment tool, can’t capture certain vital traits to ensure the proper treatment.

Thymia.ai (est. 2020 UK, $2.6m total funding), for example, has developed an interesting biometric approach to diagnosing depression and related disorders. They use video games to collect voice and facial expressions of patients, signaling when they are exhibiting symptoms linked to the behavioral patterns of someone with depression. Another exciting start-up is Alena (est. 2019 UK, $2.8m total funding), which uses neuroscience-based assessments, in the form of playing simple games, to assess how your brain works and then provide users with behavioral therapy to overcome social anxiety.

Turning our focus to treatment, we see a lot of teletherapy plays. There are full-stack approaches such as TalkSpace (est. 2011 US, $413.7m total funding) covering therapy for individuals, couples, teens, and within psychiatry also offer a medication management plan. They operate as both a B2B and D2C business but their D2C approach appears to have numerous difficulties with their conversion and retention, which tends to drive high marketing spending (5). Contrastingly, Koa Health (est. 2016 UK, $36.32m total funding) is also tackling the therapeutic and diagnostic segments but operates exclusively as reimbursable B2B. Therefore, based on our evaluation of B2B vs. D2C, we concluded the economics of D2C appear super tricky, and hence we prefer either the B2B or B2B2C business models.

“Mental health is not a destination, but a process”

Another segment in the therapeutic space that has been getting a lot of attention, albeit not always positive, is prescribed digital mental health: see HelloBetter (est. 2015 Germany, $12m total funding), offering stress and burnout courses that prescribed by doctors and therapists (reimbursable B2C/B2B2C approach). Digital therapy solutions are now reimbursable due to the introduction of DiGA in Germany (digital health applications, “Digital Gesundheitsanwendungen”): a DiGA is a CE-marked medical device. (It seems very likely that France and several other European countries will also allow for reimbursement of digital solutions in the future)

Some physicians we spoke with say that even with the DiGA “approval stamp” adoption rates will not pick up immediately as a) the system and doctors are not adequately trained on how to operate the DiGA environment, and b) it excludes a big target audience that would love to use a vetted product but do not want to go the extra step to go to the doctor’s office for a prescription.

We have seen virtual care platforms in the domains described above expanding horizontally and vertically within clinical fields. For example, Headspace (B2C) acquired Ginger (est. 2011 US $236m total funding) (B2B) for $3b in a vertical integration play, aiming to become a leading provider of digital behavioral health. Together, Ginger and Headspace will reach 100 million consumers. In turn, K Health (est. 2016 US, $278m total funding), a telehealth primary care provider, acquired Trusst (est. 2019 US), a messaging-based mental health platform, in a horizontal manner (B2C).

Record-breaking exit activity largely driven by M&A deals (2)

As can be seen from the chart above, 2021 was already a banner year for M&A exits, with 43 exits on record, an 87% increase over 2020, and we expect this trend to continue in the next 12 to 24 months given the high number of players and how fragmented the market has become (3).

Our belief is in the end, only a few players will be able to capture a large share of the overall mental health market. The success of those companies will depend on several factors: their level of scientific backing and the breadth of offerings they can provide (in this case, the direct or indirect communication to psychotherapists), and a seamless user experience.

Mental health for employees

A particular segment of digital mental health getting a lot of attention focuses on the workforce. Overall, four in ten US employees reported that their mental health declined due to the pandemic (6). No surprise then that 76% of U.S. employers increased investments into virtual care offering (7). For example, the U.S.-based Spring Health (est. 2016, $297.49m total funding) take a very data-driven approach to personalize their support for teams (from subclinical preventative to clinical treatment solutions).

In Europe: Nilo.Health (est. 2019 Germany), and Kyan Health (est. 2021 Switzerland, $1.67m total funding) cover a full-stack mental health offering for employees: from bite-sized auditory content to journaling and professional counseling services. Moka.Care (est. 2020 France, $18M total funding) place more emphasis on group therapy sessions.

From our research, we have two main observations regarding mental health for the workforce: firstly, many start-ups focus on the individual only. However, we believe that a combination of standard care for both teams and personalized tools for individuals is the best way forward. Secondly, virtual care platforms will succeed by adopting a holistic health-partnership strategy.

Younger generations

Maintaining good mental health over the last two years has been challenging, but seeking help has, for adults at least, has never been easier given the breadth of options as outlined above. Yet, younger generations, particularly children who may have suffered the most from the lack of vital social environments, do not find such a broad range of offerings, especially not in Europe. Studies show that digital mental health interventions (DMHIs) for the younger population can increase “efficiency, reach, and standardization as well as reduce costs of providing of mental health care” (8).

Coincidentally, an article by Fortune states that kids say their mental health is fine; but experts disagree (9). Kids’ self-reported responses to a survey show that of the over 1,000 kids and teens, 89% described their mental health as very good or somewhat good, and 80% said they are a little or not at all concerned about their mental health. Mental health professionals view this data as part of a multilayered and complex story, whereby there is a tendency for some kids to underreport mental health struggles, with the limited availability of mental health care feeding into this trend.

Children’s Worsening Mental Health due to Pandemic (November 2020) (10)

Some of the previously-mentioned companies in this article also target families and kids, such as subsections of Talkspace or Calm. Yet, we feel that the younger generation’s needs are vastly different from adults’ and should therefore be treated differently. For example, US Gen Z employees saw the highest percentage of declining mental health in 2021; in contrast, this was lowest among Boomers. Many Gen Z-ers were in the midst of one of their most defining chapters of life, studying at university or just having graduated and finding a completely different set-up of working environments. That is why we are excited by specialized mental health approaches such as Uwill, an online therapy platform explicitly targeting college students (est. 2020 US, $8.5m total funding).

As it relates to the content, many companies focus on sleep and relaxation tools only, and indeed there has been a massive influx of preventative mental health apps on the market. To help build trust with parents, our advice is that even preventative apps, need to conduct studies on their efficacy and leverage their pedagogical value. Trust will ultimately be the deciding factor to drive WOM user adoption, reducing the need for significant marketing spend on performance marketing or micro-influencers, the impact of which we have seen to decline over time as the company scales.

Nuances in start-up offerings for children are also important. For example, we love what Aumio (est. 2019 Germany) is doing with their content, walking kids through one coherent storyline to enable better identification with states of mind. Another prominent player is Moshi (est. 2017 UK, $23m total funding), which combines entertainment and mindfulness and has seen very good traction in the U.S. Both start-ups are highly-rated and provide a good gateway into the mental health space for young children.

Although both players are blending elements of mindfulness and entertainment, we see Moshi rather on the entertainment side and Aumio on the mindfulness end of the spectrum. Both players are thus able to capture a broad audience, but parents will need to assess what type of content their children need.

Parents will need to carefully assess DMHIs for their children

We see an unmet need targeting children on the therapeutic and diagnostic side, with only a few notable incumbents. Probably, the two most well-known are Little Otter (est. 2019 US, $26.2m total funding) and Daybreak Health (est. 2020 US, $12m total funding). Little Otter covers both the toddler to adolescent age group and the entire family, all through a very easy-to-navigate online therapy solution. Daybreak Health realized that 80% of teens with mental health needs were untreated. They partner with youth, families, and schools to create personalized, easily accessible, and affordable mental health programs by matching children with a licensed clinician.

Similar to companies targeting the workplace, DMHIs for children should target schools and educational settings to identify those experiencing or at risk of developing psychological symptoms (11). We think it is crucial to include DMHIs even without a present problem, and we would love to see it become part of school curricula. That way, we feel children will better understand what emotions or states of mind they are experiencing and can more easily identify and act on these when they arise.

Many parents struggle with their children’s mental health issues but do not know where to turn for help. Luckily, the rise of digital offerings present an opportunity to educate our children about mental health.

In summary, mental health conditions are increasing worldwide. Mental health conditions have a substantial effect on all areas of life, and WHO estimates that two of the most common mental health conditions, depression, and anxiety, cost the global economy around US$1 trillion each year. Despite these figures, global government-sponsored programs targeting mental health are less than 2% (12). It is no wonder the private sector has stepped up and we are excited to see what lies ahead.

If you know any companies targeting adolescent mental health, feel free to get in touch with us.

Published March 2022; updated August 2022.

Sources

OECD. Tackling the mental health impact of the COVID-19 crisis: An integrated, whole-of-society response. May 2021.

BBC. Depression doubles during Coronavirus. August 2020.

CB Insights. State of Mental Health Tech 2021 Report. February 2022.

Time. Insurance Claim Data Show How Much Teen Mental Health Has Suffered During the U.S. COVID-19 Pandemic. March 2021. / Time. Depression and Suicide Rates are rising sharply…

Global News Wire. Talkspace, Inc. Investors with Substantial Losses Have Opportunity to Lead Class Action Lawsuit. March 2022.

Statista. Employee Mental Health Changes Covid 19 by generation. August 2021.

Business Group on Health. Health Equity, Impact of Pandemic Among Large Employers’ Top Concerns. August 2021.

Cognitive and Behavioral Practice. Khanna, M.S., and Carper, M. Digital Mental Health Interventions for Child and Adolescent Anxiety. February 2022.

Fortune. Kids say their mental health is fine. Experts disagree. December 2021.

KKF. Mental Health and Substance Use Considerations Among Children During the COVID-19 Pandemic. May 2021.

Davies, S.M., et al. Preventative Digital Mental Health for Children in Primary Schools: Acceptability and Feasibility Study. December 2021.

World Health Organization. Mental Health. November 2021.